The elephant in the property market

John Lindeman reveals an elephant that’s making its presence felt in some property markets and explains why it’s largely going unnoticed.

One of the main drivers of housing demand has the power to radically alter housing prices and rents, yet like an elephant in the room, it’s being ignored by most analysts and researchers.

The elephant is the movement of people from one State or Territory to another, which is called interstate migration.

The biggest changes to property markets are made when people move

People change housing demand and supply when they move, because we all need a place to live. When enough people move, they can dramatically alter housing prices and rents in the process.

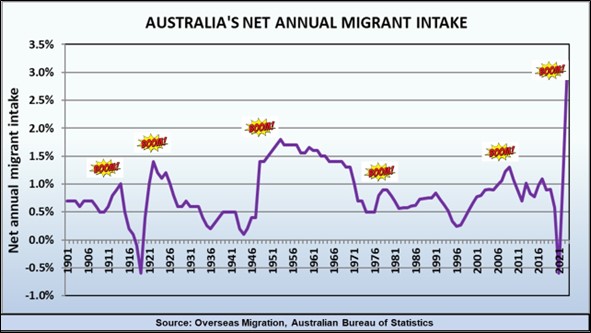

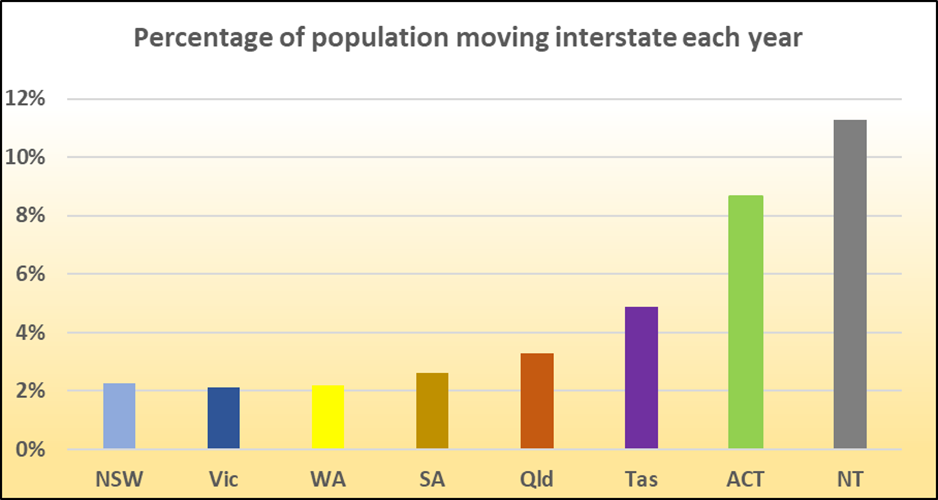

Around three percent of our total population moves from one State or Territory to another each year, but as this graph shows, the percentages of interstate movers is significantly higher in Tasmania, the ACT and the Northern Territory.

Over 11% of the Northern Territory’s population are interstate movers

The large numbers of people moving in and out of the Northern Territory each year is largely due to the presence of the huge army, navy and RAAF bases and military training facilities located there to safeguard our northern borders.

The recent strengthening of our defence capabilities in the Northern Territory has led to an increase in the number of defence personnel and their relocation in or out of Darwin, causing the current housing shortage and property market boom. Although the Northern Territory has a small net annual interstate migration figure, this hides the fact that over 30,000 people move in or out of the Territory each year. With such massive numbers of people moving, why is this phenomenon going unnoticed?

The elephant is hidden from our view

The answer is that many analysts and economists use net interstate migration numbers, which is the net increase or decrease in the population of a State or Territory from interstate movements. This is very different to the total numbers of people arriving and leaving, which is what’s actually occurring.

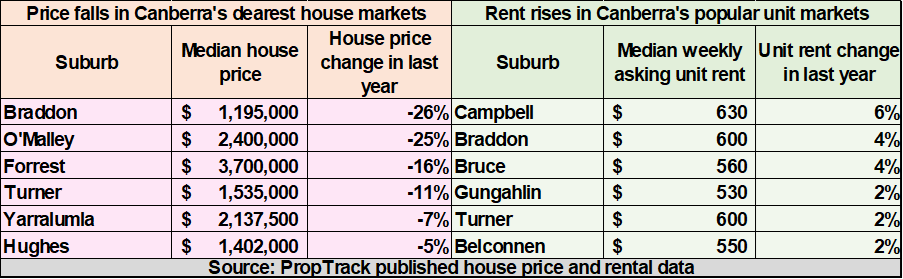

For example Canberra’s net interstate migration fall last year was only 1,300 people, but 21,500 residents left the ACT while another 20,200 people arrived, which means that over eight percent of Canberra’s population moved in or out of the Territory.

Young people are moving to Canberra from other States

Why is this important? Because the people arriving very often have different housing needs from those leaving. Most of Canberra’s arrivals are young professionals seeking work in the public service and creating demand for unit rentals, while many of those leaving are older residents retiring at the end of their careers and selling empty nests.

The impact that these movements are having on the Canberra housing market becomes clear when we compare the house price falls that are occurring in Canberra’s well established and dearer suburbs where older people are leaving, to the increases in weekly unit rents taking place in suburbs where younger people are arriving.

In fact, many of the otherwise unexplainable ways that housing markets perform becomes clear when we look more closely at who is moving interstate and why, rather than the net interstate migration figures.

Young people are leaving Tasmania for the mainland

There was a net natural increase of only 200 people in the entire State of Tasmania last year, while 15,000 people left for the mainland.

They were replaced by just 13,000 people moving to Tasmania, so it was only the 3,000 net overseas arrivals who kept the State’s population in growth.

On the face of it, these figures look terrible, with an interstate net migration drain of 2,000 people and a net increase in population of only 1,000, easily the lowest of any State or Territory.

However, the 15,000 people who move to the mainland each year are younger people in search of employment, education and lifestyle opportunities on the mainland. They leave family homes behind, creating empty bedrooms and empty nests, but not empty homes, so the housing supply doesn’t increase with their departure.

Most of the 13,000 people moving to Tasmania from the mainland, on the other hand, are older people motivated to retire there by the State’s low housing prices and milder climate. These cashed up downsizers create instant buyer demand.

So the interstate migration figures miss the elephant in the room because they don’t show us the impact of those departures and arrivals on housing supply and demand. These tell us that the rate of new housing supply is not keeping up with the demand and many locations are at the turning point.

This means that housing prices have the potential to boom, especially in the big population centres such as Hobart and Launceston and popular retiree destinations such as Devonport and Ulverstone.