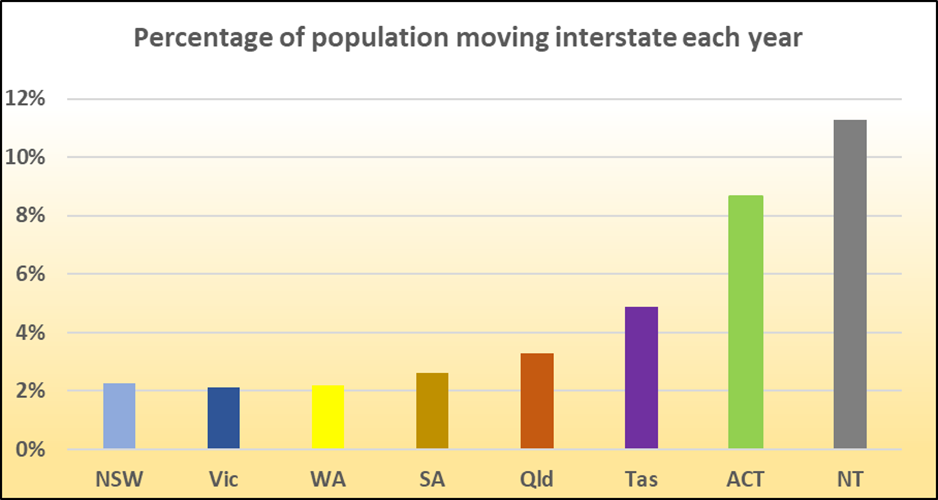

There was a net natural increase of only 200 people in the entire State of Tasmania last year, while 15,000 people left for the mainland.

They were replaced by just 13,000 people moving to Tasmania, so it was only the 3,000 net overseas arrivals who kept the State’s population in growth.

On the face of it, these figures look terrible, with an interstate net migration drain of 2,000 people and a net increase in population of only 1,000, easily the lowest of any State or Territory.

However, the 15,000 people who move to the mainland each year are younger people in search of employment, education and lifestyle opportunities on the mainland. They leave family homes behind, creating empty bedrooms and empty nests, but not empty homes, so the housing supply doesn’t increase with their departure.

Most of the 13,000 people moving to Tasmania from the mainland, on the other hand, are older people motivated to retire there by the State’s low housing prices and milder climate. These cashed up downsizers create instant buyer demand.

So the interstate migration figures miss the elephant in the room because they don’t show us the impact of those departures and arrivals on housing supply and demand. These tell us that the rate of new housing supply is not keeping up with the demand and many locations are at the turning point.

This means that housing prices have the potential to boom, especially in the big population centres such as Hobart and Launceston and popular retiree destinations such as Devonport and Ulverstone.