The Brisbane Games and property prices

We can expect many webinars, blogs, even free reports about how the Brisbane Games will turbocharge the housing market. To sort out the fantasy from the facts, property market analyst John Lindeman explains what effects the Brisbane Olympic Games could have on property prices.

After the current Olympics conclude, we’ll have the Paris Olympics in 2024 and then the Los Angeles Games in 2028. The Brisbane Olympics are a long eleven years away, but could the local property market be heading for some big changes well before construction begins, ticket sales open and spectators start arriving?

We can find the answers by looking at what took place in the Gold Coast property market as a result of the Commonwealth Games held there in April 2018.

After the completion of specially built and improved sporting, transport and accommodation venues, the economy was boosted by the arrival of local, interstate and overseas visitors. So ,what changes occurred to the property market before, during and after the Games?

Before the Games – massive infrastructure projects

Getting the Gold Coast ready for the games involved massive spending on new infrastructure, such as improving and constructing sporting centres and building the G-Link light rail to provide easy access to the venues. This naturally led to a rise in the number of construction workers, but did this then also lead to an increase in housing demand?

The facts are that most infrastructure projects do not increase housing demand at all – they create demand which is directly related to their purpose – hospitals for sick people, universities for students, shopping centres for shoppers, sporting events for spectators.

Infrastructure projects carried out in remote or captive markets tend to increase demand for rental accommodation from workers, because they need to relocate there while construction is in progress. This is not the case in major cities, because the construction work is largely carried out by local contractors who already live in the area.

This is what occurred during construction of the facilities for the Commonwealth Games, with extra workers from Brisbane and other nearby population centres commuting to and from home, rather than renting locally during the construction phase. As a result, there was little to no rise in rental or home buyer demand during the years prior to the Games.

The projects did, however, cause some disruption to retail and commercial business, especially with the building of the G-Link light rail disrupting the centre of popular tourist precincts such as Southport, Main Beach and Surfers Paradise.

In those areas, noise, dust and road closures had a negative impact on both retail and residential housing demand.

During the Games – huge boost to tourism

Over one million interstate and overseas visitors attended the Commonwealth Games, and gave the local tourist industry a huge shot in the arm. The accommodation and tourist industry such as hotels, motels, entertainment facilities, restaurants and specialist retail shops all benefitted, although the rise in demand was only temporary.

As the increase in demand was for short stay accommodation, it did not ripple through to the housing market, except for a temporary rise in accommodation services such as Airbnb.

After the Games – better facilities and more tourism

The legacy of the Games has been improved and specially built sporting venues and of course, the G-Link light rail which is gradually being extended all the way to the NSW border. There was also a rise in international tourism to the Gold Coast, especially from Commonwealth countries in 2018-19, but this quickly dissipated after the outbreak of the COVID-19 pandemic.

When looking at what effect, if any, that all this activity may have had on the local property market before, during and after the Games, it is important to realise that there are two different types of property and that they can behave very differently from each other at such times.

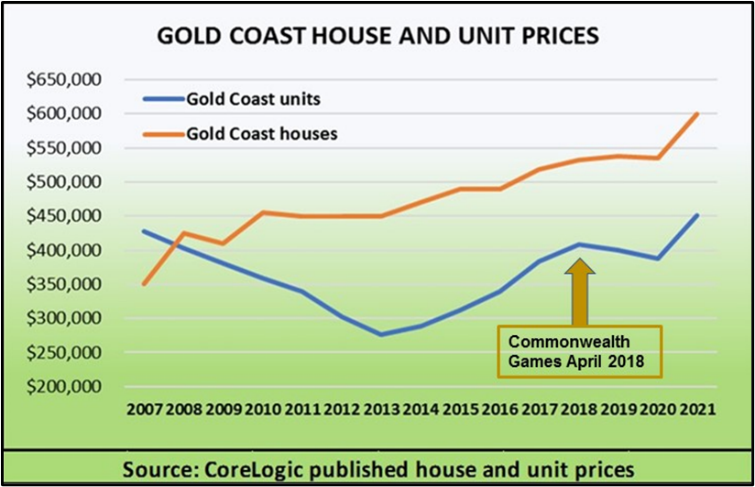

The Games had no effect on the Gold Coast house market

With well over half a million residents and two hundred thousand dwellings, the Gold Coast is the sixth biggest city in Australia, but what makes it unique is that one quarter of the city’s dwellings are units. As the graph shows, these two markets performed very differently in the years leading up to the Commonwealth Games.

Gold Coast house prices dipped slightly after the Global Financial Crisis (GFC) in 2008, but then rose slowly until another small price correction occurred as a result of the social and economic uncertainty caused by the COVID-19 pandemic.

The data shows that the Games had no apparent effect on the rate of house price growth or any other measurable impact on the Gold Coast house market.

The Games had a big effect on the Gold Coast unit market

The unit market had a very different experience. The graph shows that the Gold Coast unit market entered a sustained period of price decline after the GFC, when it was abandoned by overseas and local investors. Confidence and buyer demand returned after 2013-14, with the unit market even experiencing a mini-boom, but even so prices have only just returned to their pre GFC levels.

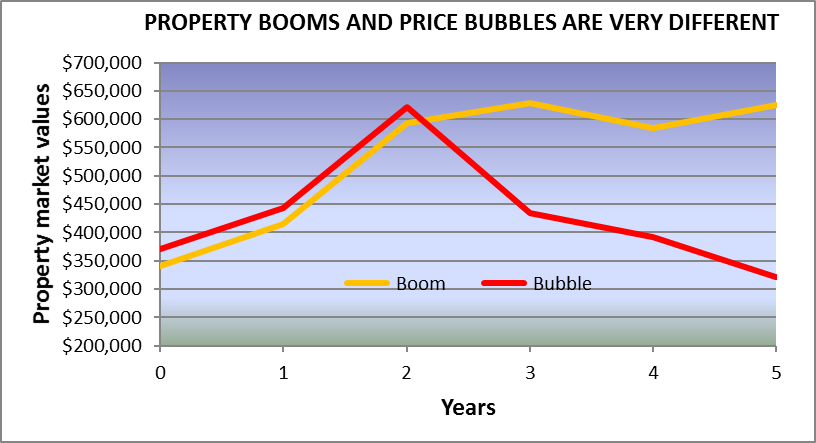

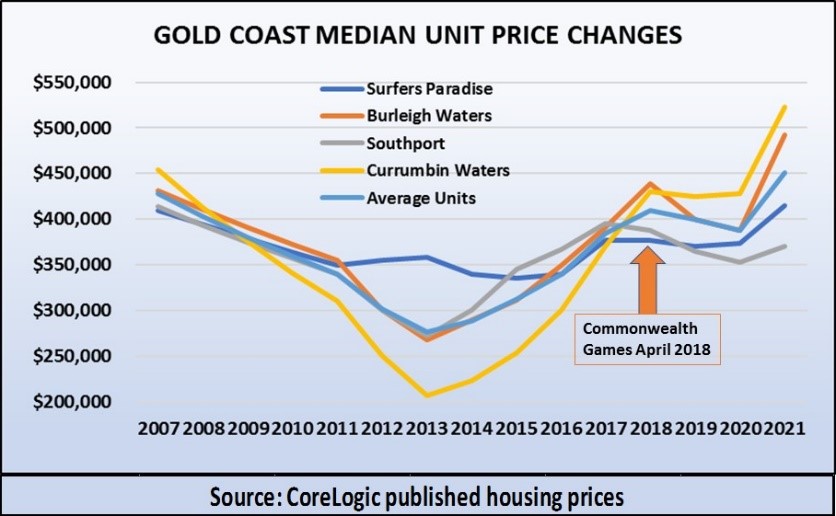

This graph shows how unit prices fluctuated before, during and immediately after the Commonwealth Games. Unlike houses, where there was no noticeable effect on prices, unit values rose steadily in the lead up to the Games, creating a bubble, bursting when the Games were over.

This picture is typical of speculative investor booms when they become bubbles and then burst when the incentive to buy property stops.

The reason that this took place in the Gold Coast unit market and did not affect house prices is because units are ideally suited to speculative investment. They can be sold off the plan in large numbers well before construction even starts and promoted to overseas and local investors with generous rental guarantees coupled with assurances of rapid and imminent price growth.

Who made a profit from the Gold Coast unit market boom?

Did any property investors profit from the Games? The data shows that unit prices on the Gold Coast, especially in suburbs such as Currumbin Waters and Burleigh Waters rose by fifty percent and more in the few years before the Games were held, so some profit taking was likely.

Based on this experience, it is possible that such a speculative bubble could form again in the lead up to the Brisbane Games in some of the city’s unit markets, but it is unlikely to have any impact on house prices.

Could investors make a profit from the Brisbane Olympics?

There will undoubtedly be a rise in speculative investment in the lead up to the Olympic Games, and unit developments are the obvious candidates. As new unit developments located near proposed Games venues are announced, speculators will quickly purchase the first available off the plan. They will then watch and wait as both local and overseas investor interest rises with the new developments being sold internationally.

Project marketers and sellers’ agents will promote them at free events and seminars with low deposit bonds and attractive rental guarantees using the glitz and glamour of the coming Olympic Games to motivate and entice purchasers.

Using the 2018 Commonwealth Games unit market experience as a guide, we can expect informed speculative investors who have purchased units a few years before the Olympic Games to offload them just before the Games begin. They will try to time their selling point just when excitement is at fever pitch and prices are at their peak.

It seems highly likely that the only real changes to the Brisbane property market caused by the Olympic Games will be from speculation. The trick will be knowing what to buy, when to buy, where to buy and most critically, when to sell. If this opportunity seems tempting, remember that the possible gain from property speculation may not outweigh the obvious potential for loss, and of course, there may be much better property investment opportunities with less risk to be found elsewhere.